The market got what it wanted last week. Oil came down. The Middle East calmed down. Treasury yields rallied. The question is whether it got what it needed.

Beneath the relief rally, a more important debate is taking place: Is inflation an energy problem, or is inflation becoming structural again? That was one of the most interesting talking points from this week’s capital markets call, and it has significant implications for CRE borrowers, lenders, and anyone waiting for rates to ease.

The market got relief. It did not get resolution.

The narrative over the last month has been straightforward. Oil surged, inflation expectations moved higher, and rates followed. Then geopolitical tensions eased, crude retraced, and Treasury yields rallied.

Normally that would be enough to improve the outlook.

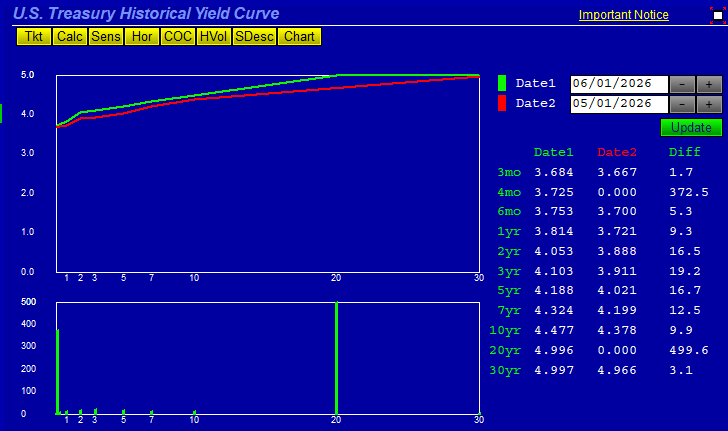

The problem is that rates remain materially above where they started May, even after the rally. The bond market appears willing to remove some geopolitical risk premium, but it is not yet willing to declare victory over inflation.

The chart below shows just how much higher rates remain across the curve despite the recent relief rally.

Source: Tradeweb U.S. Treasury Historical Yield Curve; data as of 6/1/25

Inflation has become bigger than oil.

One observation from this week’s call stood out. For most of the past year, markets have treated inflation as an energy story. Higher oil equals higher inflation. Lower oil equals lower inflation.

The economy no longer looks that simple.

Labor remains expensive. Infrastructure spending remains robust. Semiconductor and technology costs continue to rise. Supply chains continue shifting toward reshoring, friend-shoring, and domestic production. The old globalization model optimized for lowest-cost production. The new model prioritizes resiliency and security.

That may be strategically beneficial. It is also more expensive.

What the market is starting to price.

A little over a month ago, discussions about Fed hikes felt absurd. Today, they no longer do. Forward markets have not just pushed rate cuts further into the future; they have largely removed them from the curve and are now assigning some probability to hikes.

Bloomberg WIRP shows implied overnight rates rising from roughly 3.63% in June 2026 to almost 3.96% by September 2027, which is less a “delayed easing” story and more a higher-for-longer repricing. The market is no longer asking when cuts arrive. It is starting to question whether the Fed is done tightening at all.

Source: Bloomberg L.P., WIRP; data as of 6/1/25

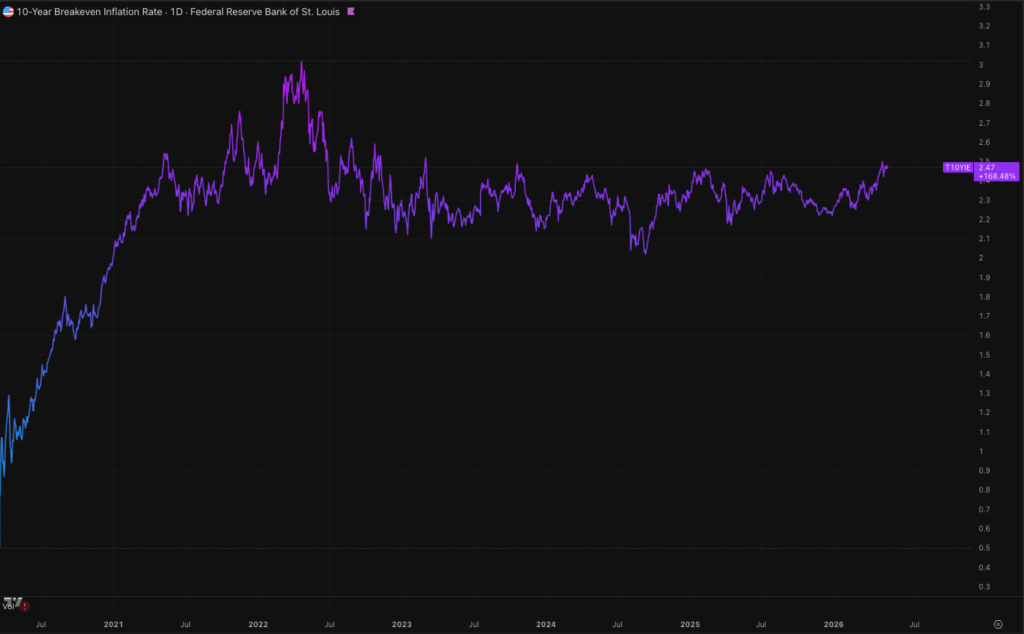

Breakeven inflation deserves more attention.

One metric we continue to watch closely is breakeven inflation. Breakevens represent the market’s implied inflation expectation over a given period. Put simply, it is the inflation rate at which investors would be indifferent between owning a Treasury bond and an inflation-protected Treasury (TIPS). When breakevens rise, the market is signaling that future inflation risk is increasing.

That is exactly what we have seen over the past several months.

Even with oil off its recent highs, the 10-year breakeven inflation rate remains elevated. The bond market is telling us that inflation concerns extend beyond energy and into broader pricing pressures throughout the economy.

Source: TradingView, Federal Reserve Bank of St. Louis (FRED)

Borrowers are no longer waiting for the Fed.

One theme that came up repeatedly during our discussion was that transaction activity continues to improve despite higher rates. That is not what most people expected.

For much of the last two years, the prevailing view was that deal activity would return once rates declined. Instead, many borrowers appear to be accepting that today’s rates may be closer to normal than temporary and are evaluating opportunities accordingly.

The conversation is gradually shifting from: “When will rates come down? To “Can this deal work at today’s rates?”

The borrowers winning today are not necessarily those with the strongest rate view. They are the ones underwriting realistic financing assumptions, understanding their interest rate exposure, and moving when economics make sense.

That shift may ultimately prove more important than the next Fed meeting.

What we’re watching.

The next major test for markets is whether inflation expectations begin to improve alongside lower energy prices. If they do, rates may finally get the confirmation needed to move lower. If they don’t, the market may be forced to confront a more uncomfortable possibility: inflation is no longer being driven primarily by a temporary energy shock, but by a broader set of structural forces that are harder to reverse.

For CRE borrowers, that distinction matters. One path leads to lower rates. The other leads to a much longer stay in a higher-for-longer environment.

House view:

- Last week’s rally improved execution levels

- It did not change the broader rate regime

- Rates are likely to remain volatile with a modest upward bias until inflation expectations show more meaningful improvement

- This remains an execution-driven market, not a wait-for-cuts market

Increasingly, the borrowers finding opportunities today are the ones adapting to current rates rather than waiting for a future that may take longer to arrive.

Luke Fuller, Director

Luke Fuller is the Director of Capital Markets at Defease With Ease | Thirty Capital, bringing 10+ years of experience in debt structuring, interest rate risk management, and capital markets execution for CRE investors. With expertise in securitization, derivative hedging strategies, and structured finance, he focuses on optimizing debt portfolios and mitigating market risk through advanced financial modeling and analytics. Luke has extensive experience in CMBS, agency, and balance sheet lending, structuring financial instruments, and executing transactions across multiple asset classes. He has advised investors, private equity firms, and REITs on interest rate derivatives, yield curve analysis, loan restructuring, and portfolio risk assessment.

Luke Fuller is the Director of Capital Markets at Defease With Ease | Thirty Capital, bringing 10+ years of experience in debt structuring, interest rate risk management, and capital markets execution for CRE investors. With expertise in securitization, derivative hedging strategies, and structured finance, he focuses on optimizing debt portfolios and mitigating market risk through advanced financial modeling and analytics. Luke has extensive experience in CMBS, agency, and balance sheet lending, structuring financial instruments, and executing transactions across multiple asset classes. He has advised investors, private equity firms, and REITs on interest rate derivatives, yield curve analysis, loan restructuring, and portfolio risk assessment.