The market is transitioning from repricing to digestion, but the direction hasn’t changed. After several weeks of moving higher, rates are no longer accelerating — but they are not reversing. Last week was a meaningful test: heavy Treasury supply, a divided FOMC decision, and key economic data. Despite that, the market largely held together. That’s the shift. It now takes a real surprise to move rates.

Last week’s data recap

- GDP: Softer

- PCE: In line

- Labor: Still resilient

- ISM: Expansion with higher prices paid

The takeaway is unchanged: growth is holding up while inflation remains sticky.

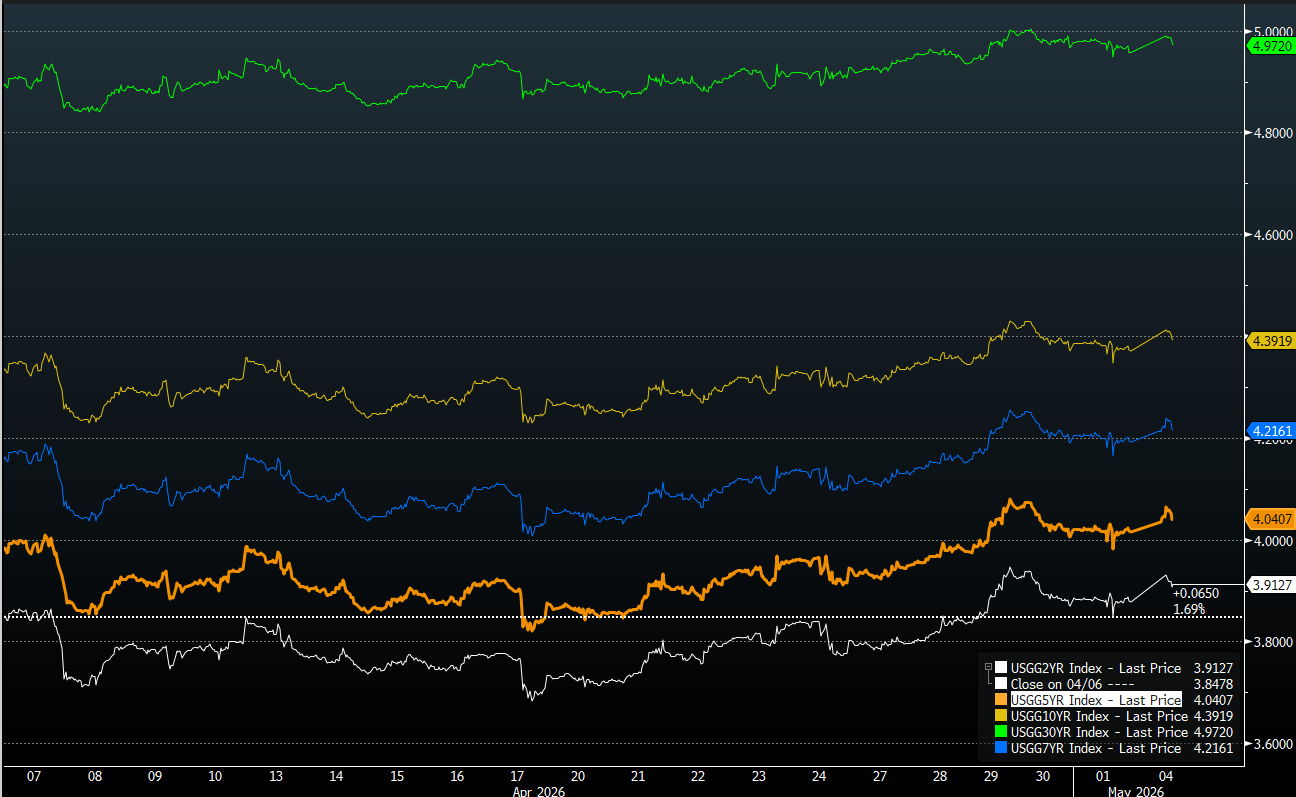

Rates are no longer repricing — they’re grinding

Source: Bloomberg Finance L.P.

The past month has been a steady move higher across the curve. The market is now digesting higher rate levels, not pricing in relief.

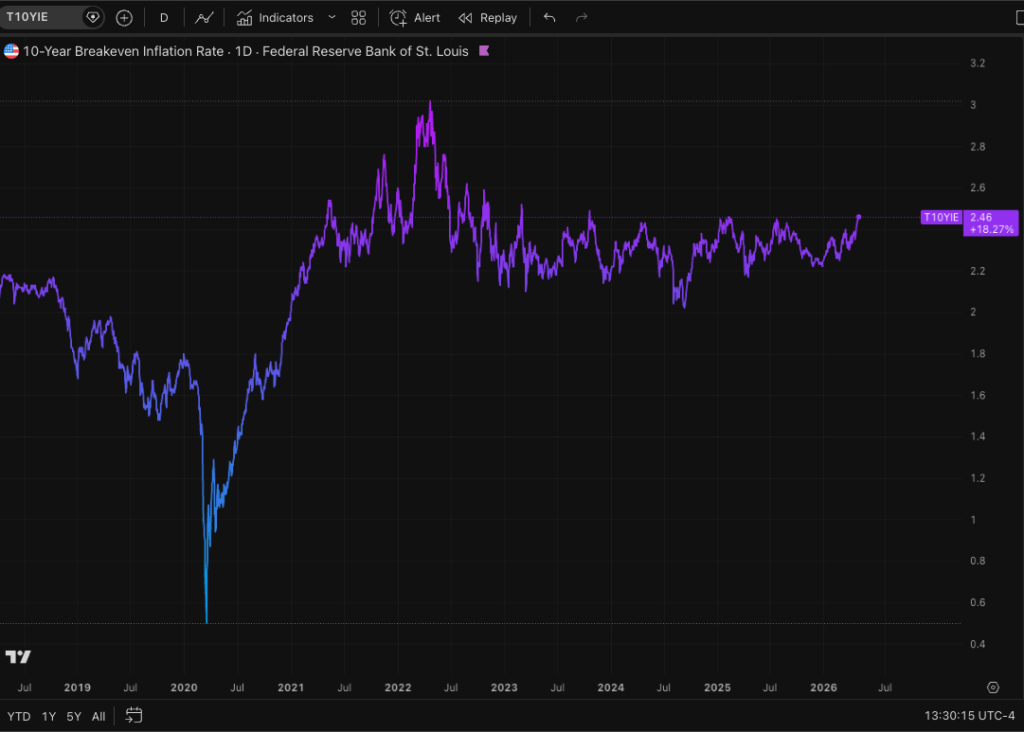

Inflation expectations are moving higher

Source: TradingView, Federal Reserve Bank of St. Louis (FRED)

Breakevens — the market’s implied inflation outlook — are drifting higher, with 5-year around ~2.7% and 10-year near ~2.5%. Rates trade off expectations, not just data. As long as expectations are rising, the long end stays under pressure.

Treasury supply showed more price-sensitive demand

Last week’s ~$180B in issuance tested demand at higher rate levels — and the market held together, but not cleanly. The 7-year auction tailed, signaling softer demand, while shorter maturities were absorbed more smoothly.

The takeaway:

- Demand remains intact, but is becoming more price-sensitive

- The market is clearing supply, but not comfortably

This reinforces the current environment — rates are not just reacting to macro, but to how much yield is required to attract buyers.

The Fed is divided

The latest FOMC outcome showed a clear split, reinforcing a market with low conviction and no clear policy path. The narrative has shifted away from a defined easing cycle toward higher-for-longer with a slight upward bias.

Borrowing costs remain elevated

Agency pricing reflects the same reality:

- Multifamily: mid–5% to low–6%

- Higher leverage: mid–6%

- Spreads: holding firm

Financing costs have not improved meaningfully. Execution still matters more than timing.

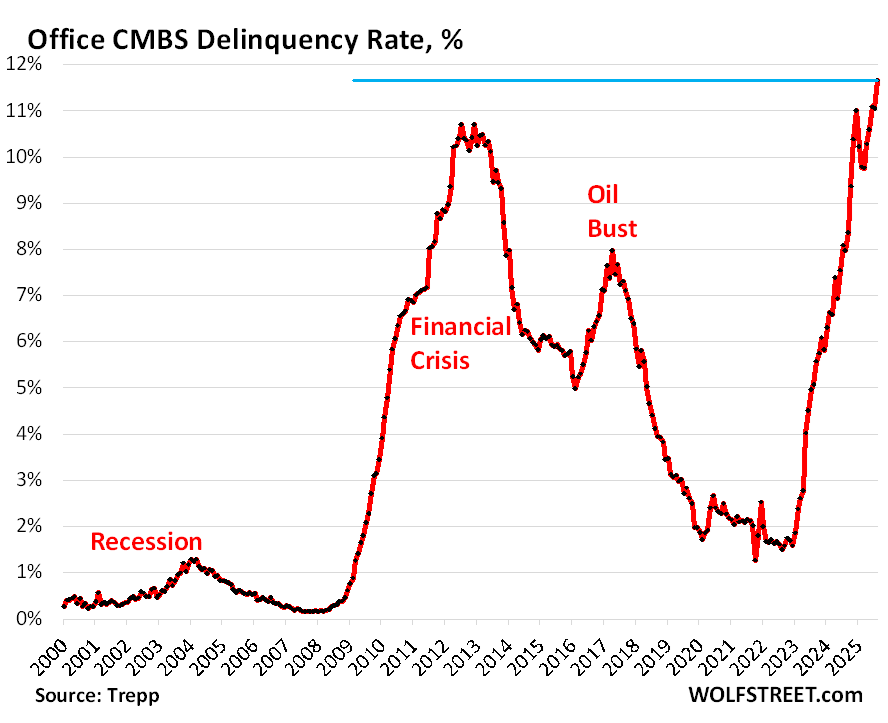

CRE stress is building

Office delinquencies are back near cycle highs. Higher rates are directly impacting refinancing, valuations, and transaction timelines.

What’s ahead this week / month

- Payrolls & Unemployment

- CPI, PPI, and PCE

- FOMC Minutes (May 20)

- GDP (May 28)

At this stage, it will take a meaningful surprise — particularly in inflation or labor — to shift the current range.

Bottom line

The market has moved from repricing to digestion, but the bias remains higher. Rates are no longer accelerating, but they are not coming down. Inflation expectations are rising, demand for duration is being tested, and borrowing costs remain elevated.

For borrowers, this is a market to manage execution — not wait for relief.

Luke Fuller, Director

Luke Fuller is the Director of Capital Markets at Defease With Ease | Thirty Capital, bringing 10+ years of experience in debt structuring, interest rate risk management, and capital markets execution for CRE investors. With expertise in securitization, derivative hedging strategies, and structured finance, he focuses on optimizing debt portfolios and mitigating market risk through advanced financial modeling and analytics. Luke has extensive experience in CMBS, agency, and balance sheet lending, structuring financial instruments, and executing transactions across multiple asset classes. He has advised investors, private equity firms, and REITs on interest rate derivatives, yield curve analysis, loan restructuring, and portfolio risk assessment.

Luke Fuller is the Director of Capital Markets at Defease With Ease | Thirty Capital, bringing 10+ years of experience in debt structuring, interest rate risk management, and capital markets execution for CRE investors. With expertise in securitization, derivative hedging strategies, and structured finance, he focuses on optimizing debt portfolios and mitigating market risk through advanced financial modeling and analytics. Luke has extensive experience in CMBS, agency, and balance sheet lending, structuring financial instruments, and executing transactions across multiple asset classes. He has advised investors, private equity firms, and REITs on interest rate derivatives, yield curve analysis, loan restructuring, and portfolio risk assessment.