Markets saw a notable shift in tone last week as a mix of softer economic data and favorable inflation readings brought some relief to interest rates and renewed optimism in key sectors.

Rates & Yield Curve

- Yields declined modestly last week, with the 2-year swap rate falling 7 bps to 3.68% and the 10-year swap down 9 bps to 3.86%.

- Despite the weekly drop, rates still ended May higher overall, with 2-year and 10-year swaps rising 31 bps and 22 bps, respectively, over the month.

- The yield curve steepening trend may accelerate in coming quarters as inflation data softens and market expectations shift.

Key Economic Data

- Consumer confidence printed strong last Tuesday, though this was contradicted by weaker Q1 consumer spending, revised down to 1.2% from 1.7%.

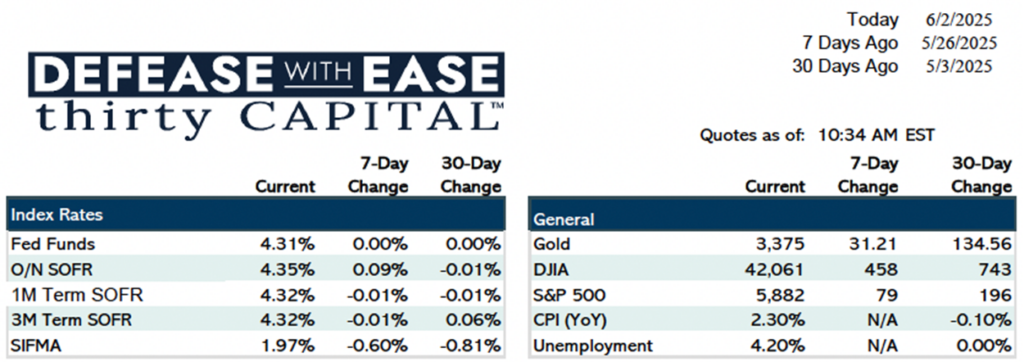

- Initial jobless claims came in above expectations at 240K, signaling a potential cooling in the labor market.

- Inflation readings were encouraging:

- Headline PCE (Fed’s preferred measure) fell to 2.1% YoY, just above the 2% target.

- Core PCE held steady at 2.5%, down slightly from the previous month.

This Week: Jobs in Focus

- A heavy slate of labor data includes JOLTS (Tuesday), ISM surveys, weekly jobless claims (Thursday), and the all-important nonfarm payrolls (Friday).

- May payrolls are expected to show 125K new jobs, down from 177K in April, with unemployment steady at 4.2%.

- Fed Governor Waller’s dovish remarks over the weekend supported rate cut expectations despite inflation risks tied to tariffs.

Cap Pricing & Rate Expectations

- Cap pricing for a 2-year 5% out-of-the-money cap remains stable at 11.5 bps, similar to 60 days ago.

- Rate cut expectations have fluctuated:

- Start of 2024: 7 cuts forecasted

- Now: Fewer than 2 expected in 2025, and under 3 for 2026

- Implied Fed funds rate for end of 2025 hovers just below 3.9%

Sector Insights

- Retail real estate remains resilient, with strong broker pipelines and continued deal activity, particularly in the drugstore segment.

- CVS deals are moving, while Walgreens and Rite Aid face uncertainty due to corporate restructuring and privatization efforts.

- Deal execution continues to face headwinds from buyer financing delays, though sentiment is broadly positive heading into summer.

Agency Market Commentary

- Little impact from the Fannie/Freddie privatization chatter or ratings downgrade headlines.

- Agency spreads remain tight, with some value seen in farm credit and homeland discount notes.

- Agencies continue to generate substantial revenue for the government, making a full privatization scenario politically complex.

Political Backdrop

- The “Big Beautiful Bill” faces opposition in the Senate over Medicaid cuts and deficit concerns.

- Expect movement by mid-summer with a looming August debt ceiling deadline.

Outlook

- With inflation moderating and labor data softening, market focus is shifting toward timing, not just quantity, of future Fed rate cuts.

- Borrowers should look to leverage current flatness in short-term rates, while closely monitoring incoming jobs data for further clues on the Fed’s path.

Jake Tillman, Senior Analyst

Jake Tillman is a Senior Analyst, Capital Markets at Defease With Ease | Thirty Capital, bringing 5+ years of experience specializing in financial modeling, debt structuring, and risk analysis for CRE transactions. He supports the execution of financing strategies, including CMBS, as well as interest rate hedging and capital markets transactions. With expertise in cash flow modeling, credit risk assessment, and market analytics, he provides data-driven insights to optimize capital structures and manage interest rate exposure. Jake assists in scenario analysis, transaction execution, and risk assessments, ensuring alignment with market conditions and client objectives. His technical background includes financial modeling, Bloomberg analytics, and structured finance evaluation.

Jake Tillman is a Senior Analyst, Capital Markets at Defease With Ease | Thirty Capital, bringing 5+ years of experience specializing in financial modeling, debt structuring, and risk analysis for CRE transactions. He supports the execution of financing strategies, including CMBS, as well as interest rate hedging and capital markets transactions. With expertise in cash flow modeling, credit risk assessment, and market analytics, he provides data-driven insights to optimize capital structures and manage interest rate exposure. Jake assists in scenario analysis, transaction execution, and risk assessments, ensuring alignment with market conditions and client objectives. His technical background includes financial modeling, Bloomberg analytics, and structured finance evaluation.