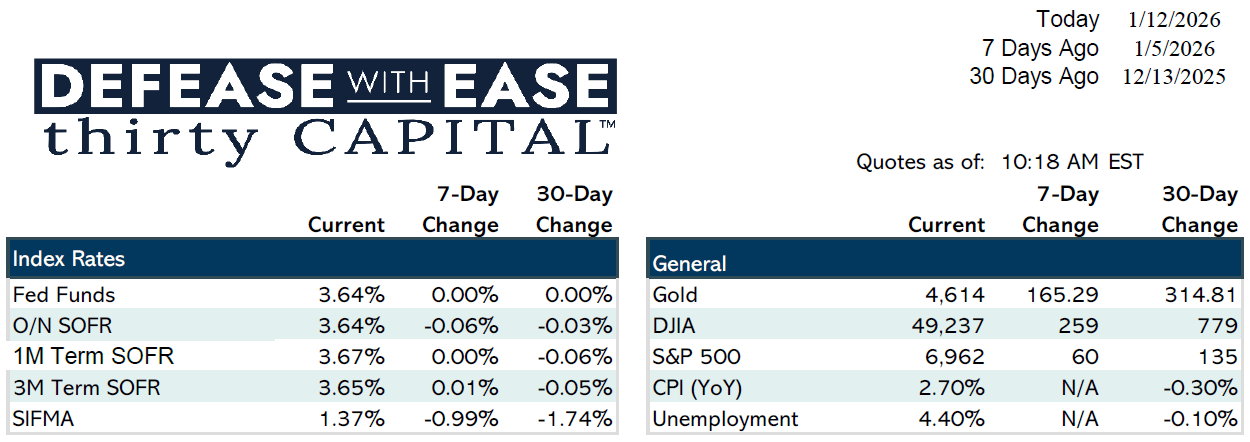

December’s jobs report signaled a cooling labor market, with payroll growth of 50,000 versus expectations of 70,000 and prior months revised down by 76,000. The three-month average has turned slightly negative, implying net job losses since October. At the same time, the unemployment rate edged down to 4.4% and wage growth remained firm, leaving the Federal Reserve in a difficult policy position. Markets have fully priced out a January rate cut, with expectations shifting toward back-loaded cuts in the second half of the year.

Treasury markets remain notably stable, with the 10-year yield trading in a narrow 3.9%–4.3% range. This stability, along with normalized credit spreads, continues to present a favorable execution window for fixed-rate borrowers.

Policy attention last week centered on former President Trump’s proposal for Fannie Mae and Freddie Mac to purchase up to $200 billion of mortgage-backed securities, effectively a form of “QE-lite” aimed at tightening mortgage spreads in an election year. Market participants expect limited near-term impact, potentially wider swap spreads, and little fundamental change to rates, noting that sustainably lower mortgage rates would still require front-end Fed cuts rather than MBS purchases alone. Execution details, funding, and timing remain unclear.

Political pressure on the Fed and uncertainty around Chair Powell’s upcoming leadership transition added to headline risk, though markets have largely looked through these developments. The prevailing outlook remains for a structurally steeper yield curve, with long-term rates unlikely to move meaningfully lower without policy easing.

On the transactional side, borrower activity is gradually picking up, with many owners focused on improving near-term NOI and positioning assets for potential sales in Q1 and Q2, which could support higher transaction volumes as the year progresses.

Looking ahead, markets will closely watch this week’s inflation data, including PPI and real earnings, for confirmation on wage and price trends. Additional personal income, spending, and PCE data later in the month could introduce more volatility as the macro picture comes into focus.

Jake Tillman, Senior Analyst

Jake Tillman is a Senior Analyst, Capital Markets at Defease With Ease | Thirty Capital, bringing 5+ years of experience specializing in financial modeling, debt structuring, and risk analysis for CRE transactions. He supports the execution of financing strategies, including CMBS, as well as interest rate hedging and capital markets transactions. With expertise in cash flow modeling, credit risk assessment, and market analytics, he provides data-driven insights to optimize capital structures and manage interest rate exposure. Jake assists in scenario analysis, transaction execution, and risk assessments, ensuring alignment with market conditions and client objectives. His technical background includes financial modeling, Bloomberg analytics, and structured finance evaluation.

Jake Tillman is a Senior Analyst, Capital Markets at Defease With Ease | Thirty Capital, bringing 5+ years of experience specializing in financial modeling, debt structuring, and risk analysis for CRE transactions. He supports the execution of financing strategies, including CMBS, as well as interest rate hedging and capital markets transactions. With expertise in cash flow modeling, credit risk assessment, and market analytics, he provides data-driven insights to optimize capital structures and manage interest rate exposure. Jake assists in scenario analysis, transaction execution, and risk assessments, ensuring alignment with market conditions and client objectives. His technical background includes financial modeling, Bloomberg analytics, and structured finance evaluation.