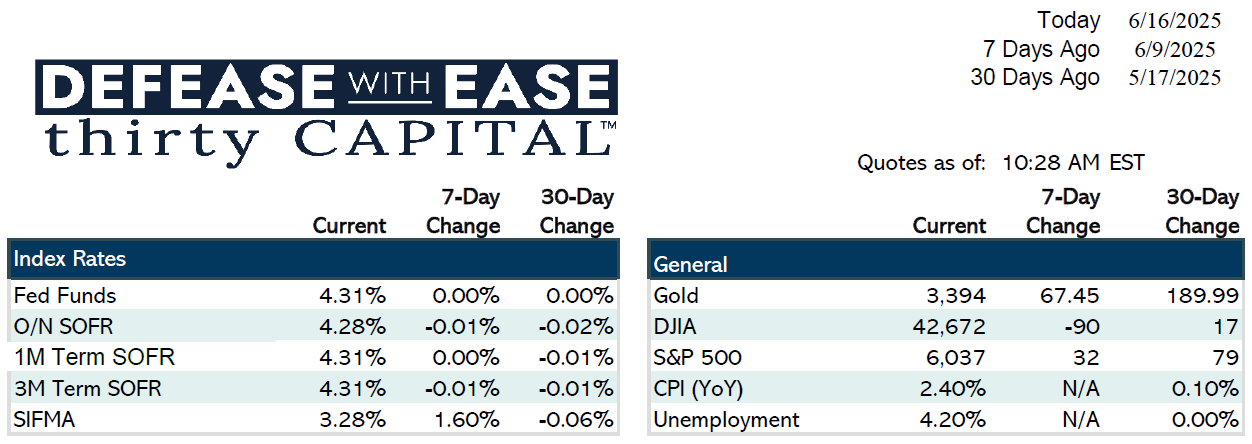

Markets rallied last week on soft inflation data and strong Treasury auctions, though geopolitical tensions reversed some of the gains into the weekend. Both CPI and PPI surprised to the downside, each printing at just 0.1% month-over-month, while jobless claims rose to 248,000 — signaling ongoing softness in the labor market. As a result, swap rates dropped 10–12 bps across the curve, unwinding the prior week’s sell-off.

Despite a strong bid for Treasuries during 2-, 7-, and 10-year auctions, Friday’s escalation in Middle East conflict pushed rates slightly higher, as markets priced in oil-related inflation risks. That upward pressure has continued into this week.

Looking ahead, the focus shifts to Wednesday’s FOMC meeting. No rate cut is expected, but updated dot plots and economic projections will shape the forward curve. The Fed’s data-dependent narrative faces pressure as inflation cools and labor weakens. Fed funds futures currently price in roughly 1.9 cuts by year-end — down from 3.15 two months ago.

Agency desks noted continued steepening of the yield curve driven more by U.S. fiscal policy uncertainty than economic optimism. On the financing side, bank debt remains dominant, with borrowers favoring short-term, interest-only structures to ride out near-term volatility. CMBS delinquencies climbed to 11%, the highest since 2013, driven largely by office and retail exposures.

Juneteenth market closure falls on Thursday this week. With central bank meetings across the globe, and U.S. retail sales data due, markets are bracing for more rate volatility.

Jake Tillman, Senior Analyst

Jake Tillman is a Senior Analyst, Capital Markets at Defease With Ease | Thirty Capital, bringing 5+ years of experience specializing in financial modeling, debt structuring, and risk analysis for CRE transactions. He supports the execution of financing strategies, including CMBS, as well as interest rate hedging and capital markets transactions. With expertise in cash flow modeling, credit risk assessment, and market analytics, he provides data-driven insights to optimize capital structures and manage interest rate exposure. Jake assists in scenario analysis, transaction execution, and risk assessments, ensuring alignment with market conditions and client objectives. His technical background includes financial modeling, Bloomberg analytics, and structured finance evaluation.

Jake Tillman is a Senior Analyst, Capital Markets at Defease With Ease | Thirty Capital, bringing 5+ years of experience specializing in financial modeling, debt structuring, and risk analysis for CRE transactions. He supports the execution of financing strategies, including CMBS, as well as interest rate hedging and capital markets transactions. With expertise in cash flow modeling, credit risk assessment, and market analytics, he provides data-driven insights to optimize capital structures and manage interest rate exposure. Jake assists in scenario analysis, transaction execution, and risk assessments, ensuring alignment with market conditions and client objectives. His technical background includes financial modeling, Bloomberg analytics, and structured finance evaluation.