Last week’s data reinforced a familiar macro setup: economic growth is slowing, but inflation remains too firm for the Federal Reserve to act decisively in the near term. Q4 GDP printed at 1.4%, well below expectations, driven by softer consumer spending and disruption from the government shutdown. Meanwhile, inflation pressures persist, with core PCE holding at 3.0% year-over-year and prices running hotter than the Fed would like.

Despite this backdrop, markets continue to price easing later this year, with roughly 2–3 rate cuts implied, largely concentrated in the back half of 2026. That said, the Fed remains firmly in “wait-and-see” mode and will require clearer confirmation from inflation and labor data before moving.

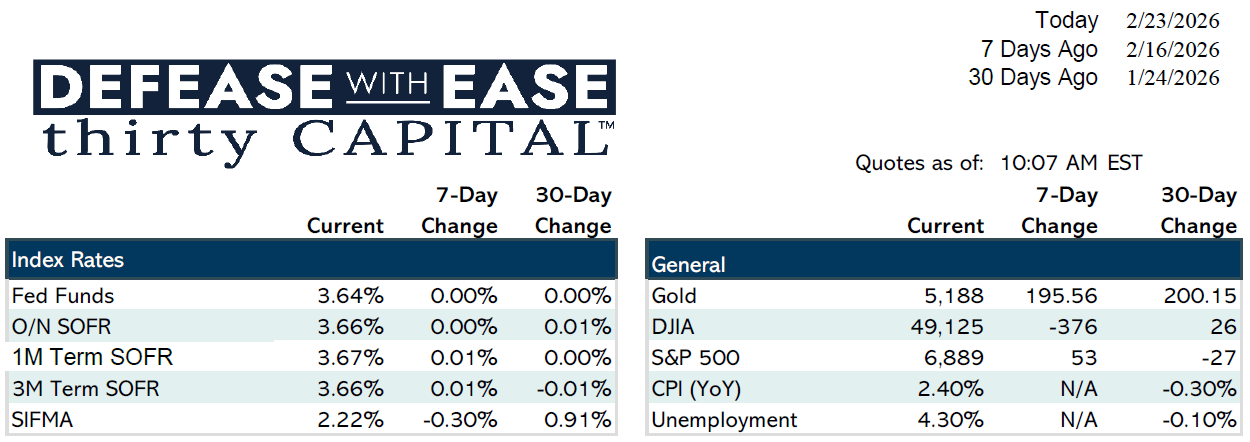

Rates & Fixed Income

Treasury yields remain range-bound amid mixed economic signals and geopolitical noise. The 10-year Treasury is hovering around 4.06%, with 4.00% acting as a key technical level, while the 30-year sits near 4.71%. Recent volatility has been driven by alternating inflation data, hawkish Fed commentary, and rising geopolitical tensions, but there has been no sustained breakout.

In agency markets, issuance remains extremely limited. With banks able to achieve near-Treasury pricing in standard auctions, there is little incentive to engage in bespoke executions, keeping activity muted for now.

Credit & Risk Sentiment

Credit spreads have widened modestly, and regional banks remain under close watch. Private credit and BDC exposure—particularly tied to data center financing—are emerging as areas of focus, as stress in those pockets could spill into broader credit markets. Equity markets have been choppy, serving as a key barometer for overall risk sentiment.

Policy & Political Noise

Markets are also digesting significant policy uncertainty. Ongoing government shutdown risks, escalating geopolitical concerns involving Iran, and confusion surrounding tariffs—following recent court rulings and new executive actions—are contributing to headline-driven volatility. While much of this is political noise, it has the potential to drive sharp, short-term market swings.

Commercial Real Estate

Stress in commercial real estate continues to build, particularly in office. Office CMBS delinquencies have climbed above 12%, the highest level since the post-GFC period. More than half of roughly $100 billion in CMBS loans maturing in 2026 are unlikely to refinance at maturity, pushing assets toward special servicing, foreclosure, or liquidation. Banks are tightening standards and showing less tolerance for extensions, while distress remains largely concentrated in office. Industrial, retail, and multifamily performance has been comparatively resilient.

Borrower Takeaways

- Near-term rate relief remains limited; optionality matters.

- Floating-rate borrowers may benefit sooner than fixed-rate borrowers as the front end of the curve responds first.

- The long end of the curve remains stubbornly elevated.

- Borrowers approaching maturity should expect stricter lender behavior and fewer extensions.

- Early modeling and proactive planning are critical—waiting for “perfect” timing may not be an option.

What We’re Watching Next

- PPI: Friday

- Jobs Report / Unemployment: Friday, March 6

- CPI: Wednesday, March 11

- FOMC Meeting: March 18

Inflation data will influence the timing of cuts, labor data will shape their pace and magnitude, and March’s FOMC meeting is expected to reinforce patience rather than signal action.

We’ll continue to monitor developments closely and will provide interim weekly updates ahead of our next formal capital markets call in early April.

Jake Tillman, Senior Analyst

Jake Tillman is a Senior Analyst, Capital Markets at Defease With Ease | Thirty Capital, bringing 5+ years of experience specializing in financial modeling, debt structuring, and risk analysis for CRE transactions. He supports the execution of financing strategies, including CMBS, as well as interest rate hedging and capital markets transactions. With expertise in cash flow modeling, credit risk assessment, and market analytics, he provides data-driven insights to optimize capital structures and manage interest rate exposure. Jake assists in scenario analysis, transaction execution, and risk assessments, ensuring alignment with market conditions and client objectives. His technical background includes financial modeling, Bloomberg analytics, and structured finance evaluation.

Jake Tillman is a Senior Analyst, Capital Markets at Defease With Ease | Thirty Capital, bringing 5+ years of experience specializing in financial modeling, debt structuring, and risk analysis for CRE transactions. He supports the execution of financing strategies, including CMBS, as well as interest rate hedging and capital markets transactions. With expertise in cash flow modeling, credit risk assessment, and market analytics, he provides data-driven insights to optimize capital structures and manage interest rate exposure. Jake assists in scenario analysis, transaction execution, and risk assessments, ensuring alignment with market conditions and client objectives. His technical background includes financial modeling, Bloomberg analytics, and structured finance evaluation.